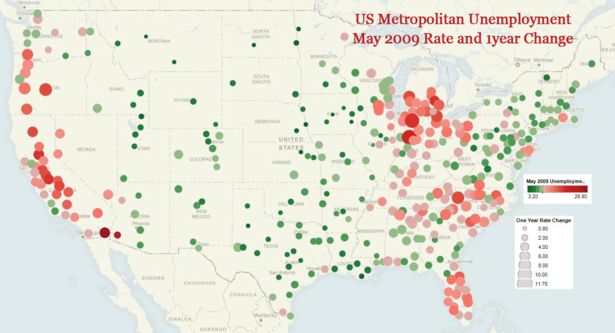

Here's a quick map of the newly released May 2009 metropolitan area unemployment numbers. On this map, color signifies the rate in May 2009 and size of bubble indicates the rate point change since May of last year. Green dots are below the national unemployment level of 9.1 in May, and red dots are above the national number.

We can see that highest unemployment is concentrated on the west coast and California, manufacturing dependend Michigan, Indiana, and Ohio, parts of Appalachia, the Carolinas, and Florida.

Unemployment is increasing the fastest in Kokomo and Elkhart-Goshen, IN; Bend, Eugene, Medford, and Portland, OR; Hickory-Lenoir-Morganton, NC; and Muskegon and Monroe, MI.

While every metropolitan area of the country saw increased unemployment over May 2008, the Great Plains from Texas to North Dakota, the Mountain West, and parts of New England are still holding employment better than the rest of the nation.

The amount of private sector jobs in Manhattan has been declining since 1958, according to the Center for an Urban Future. An increase in job-spread among the other four boroughs – Queens, Brooklyn, the Bronx, and Staten Island – has led to a shift in the New York City job market.

Still, Manhattan has the largest slice of the Big Apple job pie with a share of 61.59 % in 2008. This number has fallen about 6 percentage points over the past 5 decades. In 1958 Manhattan had a hefty 67.59% share of private sector jobs.

Needless to say, as Manhattan’s shares have declined, the other borough’s collective shares have increased overall. However, Queens has grown to eclipse Brooklyn with the second largest share in 1978 and has yet to rescind the title. Queens share of private sector jobs sits at 15.07%, while Brooklyn has a 14.09% share. From 1958 to 2008, the Bronx’s share has increased from 5.36% to 6.50% while Staten Island’s share has grown from a minute 0.75% to 2.76%.

This shift away from the city’s traditional financial sector of Manhattan can seem alarming to those not living in the Outer Boroughs. However, Manhattan-ites can take comfort in the fact that the city’s unemployment rate remains slightly lower than the national average.

Faced with an economic downturn and a bursting real estate bubble, Americans look to be staying put in greater numbers. According to Ball State demographer Michael Hicks, interviewed in an article examining the trend in the San Francisco Chronicle, "Property values have dropped so much, people can't pick up and move the way they used to."

In April, the Census Bureau reported that in 2008, the "national mover rate," declined to 11.9 percent, down from 13.2 percent in 2007. This marks the "lowest rate since the bureau began tracking these data in 1948." As William Frey, a demographer at the Brookings Institute, puts it, "the most footloose nation in the world is now staying put."

According to Frey, the middle of the decade was marked by a "mobility bubble," spurred on "by easy credit and superheated housing growth in newer parts of the Sun Belt and exurbs throughout the country". As the recession took hold through 2008, migration to suburbs and exurbs fell "flat in a hurry," showing "just how rapidly changing housing market conditions can affect population shifts."

While, as Frey suggests, people may be moving into suburbs and exurbs at a slower rate, central cities within metro areas continue to lose population. The Census Bureau reports that during 2008 "principal cities within metropolitan areas experienced a net loss of 2 million movers, while the suburbs had a net gain of 2.2 million movers." While the downturn in migration may help central cities hold onto some of their population, Frey contends that "it remains to be seen whether the migration-fueled engines of the early 2000s—especially the Sun Belt and outer metropolitan suburbs—will regain their former status."

Everybody knows we urgently need to build more homes in Britain, but how, when and where will this happen? WORLDbytes interviewed Ian Abley, an architect and manager of Audacity at the plotlands in Dunton, Essex where from the 1920s East End working class couples built cheap homes themselves. Could we do this now? Ian Abley argues we should collectively break the Town & Country Planning law of 1947 which made buying and building on redundant farmland, like the plotlands, illegal.

More information and related resources are available here.

This video and its description are derived from original content by WORLDbytes.org with the express permission of their authors. To see the original full-length video, visit this page.

As stock values go down, the value of the company pension plan investments fall with it. In good times, companies can put cash into the plans to make up the short fall. But with all the financial turmoil around us now, companies don’t have the cash and are unable to borrow it. Some companies are capping payouts and some are offering lump-sum payouts instead of, or in combination with, monthly payments. Other companies are abandoning traditional pensions – where the payouts are defined in advance of retirement – for 401(k) plans – where the contributions are defined instead and the payouts are left uncertain. That puts the risk of bad investments and market collapses on the backs of the workers instead of the companies.

For employees who are in traditional pension plans, the Pension Benefit Guaranty Corporation (PBGC) was created in 1974 to insure pensions. If your employer goes bankrupt, your pension could still be OK if the plan pays insurance premiums to PBGC. However, the coverage is limited to $54,000 a year for workers who retire at age 65, less if you retire early. The PBGC’s investment assets went down 12 percent between September 2007 to September 2008 (latest financial statements available). That’s on top of a large (albeit falling) deficit of $11 billion (their liabilities are greater than their assets). This is the company that is supposed to protect your pension if your company goes into bankruptcy. Technically, they can’t meet today’s obligations…

If your employer is in financial trouble and you are expecting to earn more than the pension insurance will cover you may need to think about working during retirement to make up the difference. According to an article published by Wharton in 2007, the Senior Citizens Freedom to Work Act “repealed the Social Security earnings limit, allowing workers 65 through 69 to earn income without losing Social Security benefits.” Good thing, too. Looks like they’ll need to keep working to make it through the depression.

Infinite Suburbia is the culmination of the MIT Norman B. Leventhal Center for Advanced Urbanism's yearlong study of the future of suburban development. Find out more.

Books

Authored by Aaron Renn, The Urban State of Mind: Meditations on the City is the first Urbanophile e-book, featuring provocative essays on the key issues facing our cities, including innovation, talent attraction and brain drain, global soft power, sustainability, economic development, and localism.